India has been the fastest-growing major economy for the third successive year. Despite global headwinds, including geo-political realignment, India’s economy would continue its strong and resilient growth of 6.7% in FY 2024 and 6.2% in FY 2025. The first Advance Estimates of National Income 2023-24 placed macro-economic growth at 7.3% in FY 24 vis-a-vis 7.2% last year. However, the nominal GDP growth is estimated at 8.9% as against 16.1% in FY 23. These figures could change following improved data coverage, actual tax collection and expenditure on subsidies, etc.

A renewed capex cycle, a well-capitalised banking system, robust credit growth, an upturn in the housing sector, rising domestic consumption, robust investment, growing services exports and “digitalization-driven productivity gains” are force multipliers. India would consolidate its global heft by important transformative drivers both on the demand and the supply sides.

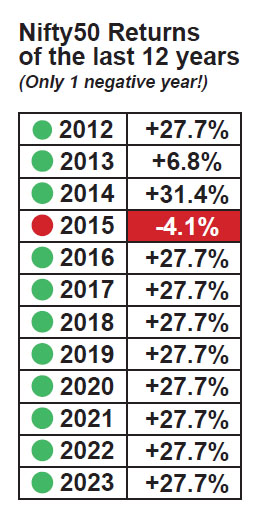

Despite external headwinds, both the Nifty 50 and BSE Sensex recorded hefty gains, making 2023 their second-best year since 2017. While Nifty surged by 20% in 2023, this was no flash in the pan, no “happenstance, … coincidence” (as Ian Fleming said through his immortal character James Bond in his novel Goldfinger). For, if the Nifty decadal returns are placed in a proper historical and comparative perspective, Nifty returns oscillated from a massive 31.4% in 2014 to a low of 3% in 2016 (with negative 4.1% returns in 2015) during the twelve-year period 2012 to 2023.

The Nifty recovered from 16,828 points in March to reach over 21,800 (28% rise), while the Sensex surged 11,000 points (18% throughout 2023), thereby breaching the 72,000 level reflecting the broader market’s strength. Further, the Nifty Smallcap 100 surging by an impressive 54%, and the Nifty Midcap 100 jumping over 44%.

The Nifty recovered from 16,828 points in March to reach over 21,800 (28% rise), while the Sensex surged 11,000 points (18% throughout 2023), thereby breaching the 72,000 level reflecting the broader market’s strength. Further, the Nifty Smallcap 100 surging by an impressive 54%, and the Nifty Midcap 100 jumping over 44%.

Indian equity markets invested `15,100 crore a month via MF SIPs in 2023 on an average, while 26.8 million new demat accounts till November showed large direct retail participation. Foreign investors first withdrew during the year but came back strongly to infuse the highest-ever `1.75 lakh crore, exceeding 2020’s `1.73 lakh crore.

This Nifty rise of 20 % in 2023 needs to be seen against the backdrop of 28.2% rise in Japan (Nikkei), 22.3% in Brazil (IBOV), 20.3% in Germany (DAX), 18.7% in Korea (Kospi), 16.8% in France (CAC), 13.8% in USA (Dow) and 3.8% in UK (FTSE). There was, however, 0.3% contraction in Singapore (STI), 3.7% in China (Shcomp) and 13.8% in Hong Kong (HSI). No wonder, then, India’s market cap-to-GDP ratio zoomed from 23% in December 2001 to 112% in March 2023. India’s stock market did well this year, with indices hitting record highs. Despite the S&P BSE Sensex ending 168.66 points lower at 71,315.09 on December 18, 2023, India’s stock market has been on a roll.

This paradigm shift induced Goldman Sachs’ report of Sept. 19, 2023 to justifiably maintain that India’s aggregate stock market value is set to rise from $3.5 trillion currently to over $5 trillion by 2024. India thus became the fifth largest in the world by market capitalization, surpassing the U.K. and the Middle East. This stemmed from three basic trends and tendencies underpinning strong macro momentum: Indian start-ups have raised $10 billion through IPOs so far this year- exceeding the sum raised in the last three years and more importantly, the pipeline for future public listings remains robust over the next two years. Hence, there is a distinct possibility that 150 private firms could potentially list on the stock market over the next 36 months, adding a whopping $400 billion of market value over the next 2-3 years. This tectonic shift, this rekindling of “animal spirits” could herald a new era for the entire ecosystem. Zomato could be quickly followed by Paytm, Ola, and Flipkart leading to a sustained bull run. Thus India’s stock market has been on a roll. But the best is yet to be both because of global cues and domestic macroeconomic drivers!

Globally, India’s economy is the fastest growing among major economies on the back of growing demand, moderate inflation and stable interest rate regime. This makes India an out-performer and with steady growth of 6% over the medium-term, equities are likely to march northwards. On top of over 20% corporate earnings this year, corporate earnings are likely to rise further over the next six months. Other strands of this debate include India’s manufacturing PMI rising to 56 in November 2023 (the 29th successive month of rise in factory activity) from October’s 8-month low of 55.5 and net FPI inflows of US$ 24.9 billion (up to Dec. 6, 2023) as against net outflows in the preceding two years. FPI Flows would be influenced by peaking U.S. dollar, the high-octane May 2024 elections and India’s greater heft in global markets. Hence, investors should stay invested despite occasional dips and troughs. As John F. Kennedy stressed way back in October 1963, “a rising tide lifts all boats”. While the big picture is unmistakably clear, a granular examination reveals a capital market divide with small-caps and mid-caps outperforming large-caps. It needs no clairvoyance to perceive irrational exuberance, bubble and unsustainably frothy valuations of mid-caps and small-caps (while Nifty gained 20% in 2023, Nifty midcap surged ahead at 39% small caps zoomed by 48%) as also, inter-alia, reflected in a significantly higher price-to-book ratio than the long-term average in the Indian capital market. Consequently, a correction, particularly in the small-cap and mid-cap space cannot be ruled out. Given this scenario of a skew in the bourses and the possibility of a decrease in India’s over-allocation in investors’ emerging market portfolios, large-caps inspire greater confidence since they possess competitive advantage, sustainable growth potential and are reasonably valued vis-à-vis mid/small-caps.

Perils of investing in Futures & Options (F&O)-Dangers Galore

Creating huge money swiftly has always lured investors to the stock markets. But a headlong dive into the F&O quicksand without fully understanding the stock market operations and information regarding companies, securities and prices can be quite catastrophic. This assumes greater significance because the SEBI’s study revealed that 89% of individual traders (i.e., 9 out of 10 individual traders) in equity F&O segment incurred losses, with an average loss of `1.1 lakh during FY22, whereas, 90% of the active traders (indulged in trading frequently) incurred average losses of `1.25 lakh during the same period. This is quite scary. It is manifestly clear that there is a free fall here like in the case of an aircraft crash when you fall from 35,000 feet. And the F&O segment sends the investors straight to the ventilator- no nursing, no treatment, no OPD, no hospitalisation or even no ICU! Tauba, tauba!

Creating huge money swiftly has always lured investors to the stock markets. But a headlong dive into the F&O quicksand without fully understanding the stock market operations and information regarding companies, securities and prices can be quite catastrophic. This assumes greater significance because the SEBI’s study revealed that 89% of individual traders (i.e., 9 out of 10 individual traders) in equity F&O segment incurred losses, with an average loss of `1.1 lakh during FY22, whereas, 90% of the active traders (indulged in trading frequently) incurred average losses of `1.25 lakh during the same period. This is quite scary. It is manifestly clear that there is a free fall here like in the case of an aircraft crash when you fall from 35,000 feet. And the F&O segment sends the investors straight to the ventilator- no nursing, no treatment, no OPD, no hospitalisation or even no ICU! Tauba, tauba!

Given the significant risks and dangers inherent in these investment instruments, Ms. Madhabi Puri Buch, SEBI’s Chairman stressed the significance of a strategic and cautious approach to investment. As she pithily said, “if you invest for the long term, you will rarely go wrong”. With such terrifying educative series, most persons shouldn’t touch F&O with a barge pole unless of course they are overpowered by an all pervading sense of greed. Greed and fear constitute the eternal flaws here- something like the “original sin” of eating the Apple by Adam and Eve.

Pathway to the Future

The Sensex correction on January 23, 2024 was not entirely unexpected. In line with our prescient forecasts, the Sensex fell over 1000 points to end at 70,371; NIFTY fell by 1.5% to close below 21,250. A deeper fall of 3% was seen in mid and small cap indices. The capital market dip triggers were disappointing HDFC results, downgrading of RIL, stricter SEBI norms on beneficial owners with effect from February 1, net selling by FIIs, profit booking across sectors and fragile 22,000 NIFTY basis. The market capitalisation of all BSE-listed stocks fell to `366.3 lakh crore. Despite such steep dip, the long run Indian growth story in general and the capital market in particular continues to be robust and positive. There could, however, be occasional hiccups. William Shakespeare wrote in his play A Midsummer Night’s Dream, “the course of true love never did run smooth”. Similarly, the capital market never progresses in a linear and progressive unidirectional manner.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.