The central banks across the world were largely on a rate hiking spree for the most part of 2022 and 2023. But given the transformed ground-realities, the evolving course of monetary policy has evoked widespread debate across the development spectrum. Some of the main strands of this debate relate to the impact of hiking interest rates, behaviour of workers, firms and consumers. There are also grave geopolitical risks and if the Israel-Hamas conflict leads to a full-fledged regional conflagration in the Middle East, it will cripple the global economy.

REPEATED RATE HIKES POST MARCH 2022

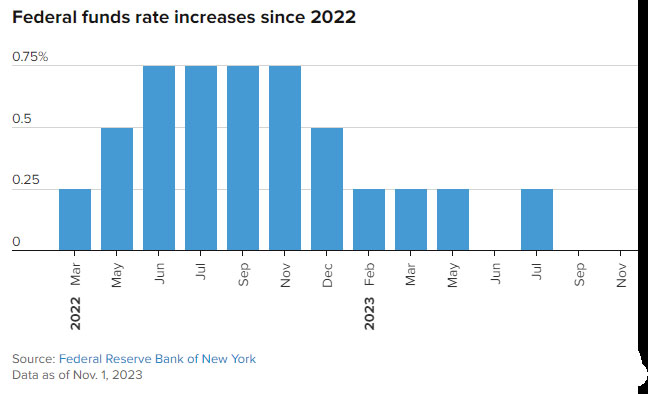

The US Fed has aggressively raised interest rates 11 times post March 2022, including four in 2023, to check the inflationary spiral. The Fed Reserve’s strategy to check inflation rests on the use of its various tools, e.g., Fed funds rate for 2% long term inflation. “Persistent inflation” stems from demand-supply imbalances and expansionary policy of the Fed and the US Government. Inflation hurts consumers, particularly low income families and fixed income groups. The Fed Reserve raised key short-term interest rates repeatedly but with limited success because of “sticky” inflation. There has to be a focus on avoiding hard-landing and greater fiscal-monetary coordination. High government spending could complicate matters.

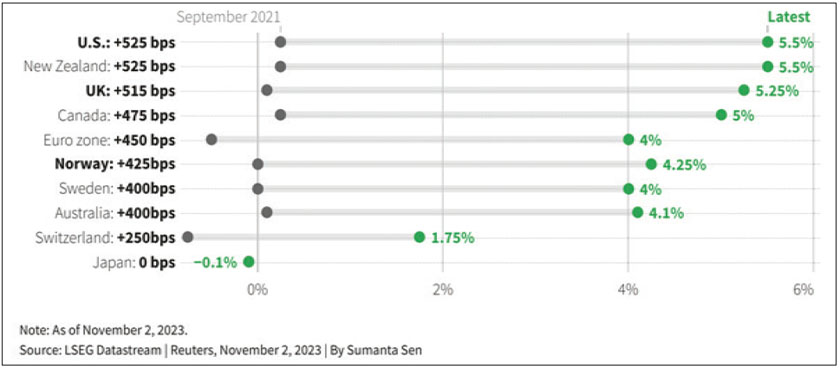

Such interest rate hikes are part of a global pattern. This thesis can be substantiated by the fact that nine developed economies (with Japan being the notable exception) raised rates by a combined 3,965 basis points (bps) in a cycle that started in September 2021.

The resilience and robustness of the US economy despite a slew of rate hikes unprecedented in four decades surprised several analysts.

US FED’S NOVEMBER POLICY ACTION

Against this backdrop, the Federal Open Market Committee (FOMC) on November 1, 2023 kept the rates unchanged for the second consecutive time at 5.25% to 5.5% range (i.e., the highest level in 22 years), where it has been stuck since July 2023. This decision, which occurred against the canvas of a growing economy and labor market and inflation well over the central bank’s target, marked a careful move “to address both the risk of being misled by a few good months of data, and the risk of over-tightening”. It also gave policymakers time to “assess additional information and its implications for monetary policy”.

The traction in the economy is manifested in the growth in gross domestic product (GDP) of the US at an annualised rate of 4.9% in Q3 and nonfarm payrolls growth totalled 336,000 in this quarter. Hence the US central bank justifiably maintained “economic activity expanded at a strong pace in the third quarter”.

Meanwhile, the US labour costs rose significantly in the September quarter amid strong wage growth. In terms of the Labor Department’s Bureau of Labor Statistics data, the Employment Cost Index (ECI), the broadest measure of labour costs, rose 1.1% in July-September 2023 after rising 1% in April-June 2023.

The personal consumption expenditures price index (PCE) rose 3.4% in September and the core PCE price index rose 3.7%. Over 3% inflation strongly suggests that inflation management will endure and rate cuts may still be some distance away.

Resilient economic growth provides comfort to the Fed in keeping interest rates high for some time. But there are also issues of the probable timing of the reversal of the rate hike cycle, the Fed’s perception on the job markets, inflation and economic growth and the lagged effect of the cumulative impact of rate hikes on the economy and corporate world.

While the July hike may have been the last in this cycle, financial and geopolitical risks buttress the higher-for-longer stance. The Fed may be close to the end of its rate-hiking cycle but a hike in December 2023 is not entirely ruled out should crude oil prices spike.

MACROECONOMIC IMPACT ON INDIA

The transmission of the Fed’s policy on the Indian markets occurs through Exchange Rate Channel, which strengthens the US dollar against other currencies, including Indian rupee and raises the debt servicing costs for Indian borrowers for loans in foreign currency; Capital Flow Channel, which reduces the interest rate differential between the US and India making India less attractive for foreign investors seeking higher returns and could lead to capital outflows from India’s equity and debt markets, thereby lowering asset prices and increasing volatility; Inflation Channel by raising the imported inflation because of the higher cost of imported goods such as oil, gold and electronics and higher domestic inflation by raising input costs for various sectors such as agriculture, manufacturing and services; Growth Channel by decelerating global growth negatively impacting India’s exports and external demand and reduced domestic demand and investment.

Data crunching reveals one-month non-deliverable rupee forward at 83.28; onshore one-month forward premium at 4.75 paisa, dollar index falling to 105.50, Brent crude futures at $79.9 per barrel, Ten-year U.S. note yield at 4.48%, foreign investors sold a net $37.5 million worth of Indian shares on Nov. 7 and foreign investors bought a net $179.2 million worth of Indian bonds on Nov. 7, 2023.

Data crunching reveals one-month non-deliverable rupee forward at 83.28; onshore one-month forward premium at 4.75 paisa, dollar index falling to 105.50, Brent crude futures at $79.9 per barrel, Ten-year U.S. note yield at 4.48%, foreign investors sold a net $37.5 million worth of Indian shares on Nov. 7 and foreign investors bought a net $179.2 million worth of Indian bonds on Nov. 7, 2023.

While Asian currencies buoyed by dropping U.S. yields post the Fed Policy rose, the Indian rupee was unchanged. But the falling oil prices and sliding U.S. yields contained the upside pressure (in USD/INR).

Brent crude on November 8, 2023 fell below $80 a barrel for the first time since mid-July on concerns of receding demand in the U.S. and China. Given that India predominantly imports oil, falling oil price augurs well for India. As of November 2, India’s average crude oil basket price was $87.09 per barrel, slightly lower than the October average of $90.08. Morgan Stanley’s note stressed that if oil prices sustainably rise to $110 per barrel, it could strain India’s macroeconomic stability, inducing the RBI to resume its rate hike cycle.

The 10-year U.S. yield dropped below 4.50%, reaching the lowest in more than a month and is now down more than 50 basis points from its recent high. The Fed Chair suggests greater flexibility on economic forecasting during times of ‘unpredictable shocks’, but this guidance did not identify the US economy growth risks.

The IMF has demonstrated that India has high debt but risks are moderate since India’s current debt is 81.9% (China 83%) of GDP. Unlike China, India’s debt is likely to fall to 80.4% in 2028 because of high growth, long debt maturities, large domestically held debt and denoted in home currency. Rising US Fed rate result in foreign investors selling out from the Indian stock markets as Indian markets become far less attractive for them. The rate hike also positively impacts US treasuries’ yield, which motivates foreign investors to pull their money out of the Indian markets and invest it in their own country. Secondly, higher interest rates leading to a weaker rupee vis-a-vis the dollar capping foreign investors returns on their investments. Thirdly, though foreign investors with a long-term horizon look beyond marginal rate hikes, small-term investors retreat because volatile market together with a weaker rupee requires hedging the positions, cutting short the returns. Higher interest rates also raise borrowing costs.

Pathway to the Future

Where do we go from here? Going forward, the disconcerting macro-economic complexities, such as, tighter financial conditions faced by households and businesses, inflation still to reach 2% on a sustained basis despite the perceptible decline in inflation from its four-decade peak last year, to 3.7% on an annual basis, the need to calibrate an economy outperforming expectations, and the hawkish tone and tenor of the Policy, our sense is that the Fed would adopt a status quoist Policy in their next meeting on December 12-13, 2023. Despite cognizable dilemmas, we do maintain that rate cuts would occur in 2024.

The Fed reaffirmed its commitment to achieving its dual mandate of maximum employment and price stability. In pursuit of this dual mandate, the Fed’s data-driven and evidence-based policy would be influenced by the data and information on issues such as the Consumer Price Index (CPI), payrolls, and GDP growth.

The domestic equity market was not impacted significantly in the wake of leaving the benchmark interest rates unchanged since market participants had already factored in the effects of these record interest rates. JPMorgan’s Pedro Martins maintains India has the strongest nominal GDP compounding among emerging markets because of demographic trends and investments in infrastructure. Two salient features in the Indian equity market are as China’s real GDP growth slows down, India is delivering a stronger GDP than China and some pension funds in the U.S. are reallocating their investments with India being the largest recipient, the others being Indonesia, Saudi Arabia and Mexico.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.