Given the pressure on forex reserves and the volatility in the value of the rupee, there has been a strategic move by the Government of India (GoI) with trade settlements bilaterally with select countries in our domestic currency. This move received an impetus post the sanction of US and allies on Russia and removal of certain selected Russian banks from SWIFT operations due to its war with Ukraine.

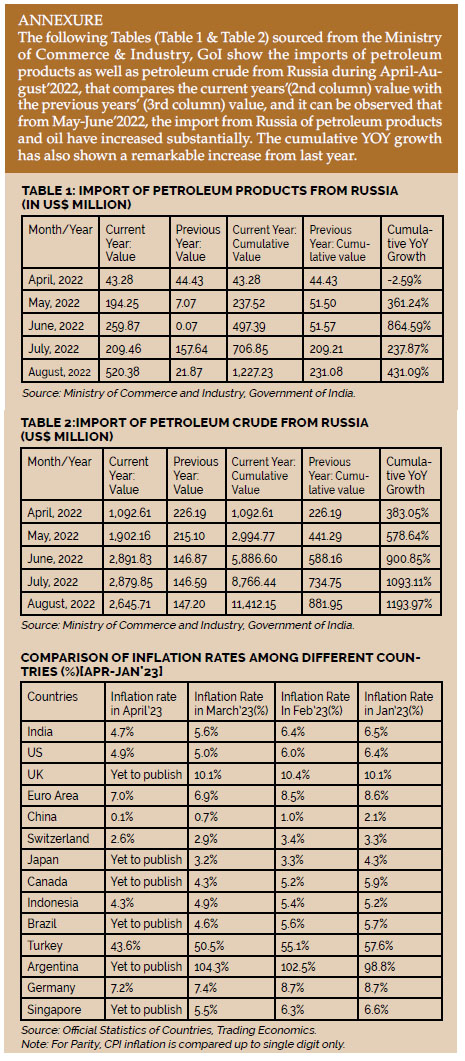

India increased its dependence on discounted Russian oil, and India’s bilateral trade with Russia between April and August 2022 surged to a record high $18.2 billion. As a trading partner also Russia’s position with India enhanced to the seventh position compared to its 25th position last year, primarily driven by rapidly rising import of oil and fertilizers in the aftermath of the Ukraine war. For instance, in 2022 so far, fuel and fertilizers- these two items constituted over 91 per cent bilateral trade between India and Russia. Russian oil is also relatively cheaper compared to countries like Venezuela. Further, Russia provided huge discounts to other countries including India during the period of sanctions imposed by US and other countries in Russia.

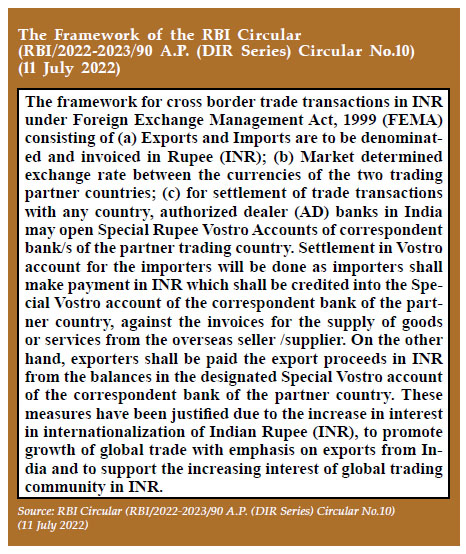

The RBI has allowed invoicing and payments for international trade in Indian Rupee vide A.P (DIR Series) Circular No. 10 RBI/2022-2023/90 dated 11.07.2022 on “International Trade Settlement in Indian Rupees (INR)”. According to the Circular, all exports and imports under the arrangement may be denominated and invoiced in Rupee (INR) and the settlement of trade transactions under the arrangement shall take place in INR. RBI has put in place the arrangement to promote growth of global trade with emphasis on exports from India and to support the increasing interest of global trading community in INR. The framework put in place by RBI is applicable for any partner country seeking to undertake trade with India in INR in terms of RBI’s Circular dated 11.07.2022. in terms of Para 10 of the Circular, the approval process is that for opening of Special INR Vostro accounts, banks of partner countries may approach Authorised Dealer (AD) banks in India which may seek approval from RBI with details of the arrangement. The AD bank maintaining the Special INR Vostro Account is required to ensure that the correspondent bank is not from a country or jurisdiction in the updated Financial Action Task Force (FATF).

The RBI has allowed invoicing and payments for international trade in Indian Rupee vide A.P (DIR Series) Circular No. 10 RBI/2022-2023/90 dated 11.07.2022 on “International Trade Settlement in Indian Rupees (INR)”. According to the Circular, all exports and imports under the arrangement may be denominated and invoiced in Rupee (INR) and the settlement of trade transactions under the arrangement shall take place in INR. RBI has put in place the arrangement to promote growth of global trade with emphasis on exports from India and to support the increasing interest of global trading community in INR. The framework put in place by RBI is applicable for any partner country seeking to undertake trade with India in INR in terms of RBI’s Circular dated 11.07.2022. in terms of Para 10 of the Circular, the approval process is that for opening of Special INR Vostro accounts, banks of partner countries may approach Authorised Dealer (AD) banks in India which may seek approval from RBI with details of the arrangement. The AD bank maintaining the Special INR Vostro Account is required to ensure that the correspondent bank is not from a country or jurisdiction in the updated Financial Action Task Force (FATF).

The Directorate General of Foreign Trade (DGFT) has introduced a provision in the Foreign Trade Policy vide Notification No. 33/2015-20 dated 16.09.2022, to allow for International Trade Settlement in INR, i.e., invoicing, payment, and settlement of exports / imports in Indian Rupees in sync with RBI’s Circular dated 11.07.2022. Further changes have been introduced in the Foreign Trade Policy vide DGFT’s Notification 43/2015-20 dated 09.11.2022 and Public Notice 35/2015-20 dated 09.11.2022 for grant of exports benefits and fulfilment of Export Obligation for export realisations in INR as per RBI guidelines.

An important benefit for the trade settlement in rupee is that it reduces currency risk for Indian players (businesses, traders, entrepreneurs, etc.). Also, the RBI needs to be less concerned about its composition of the foreign currency assets in the foreign exchange reserves, as a substantial share of trade can be settled via the domestic currency.

However, a caveat would be less autonomy in monetary policy manoeuvring by the Central Bank according to the requirement by the domestic economic situations, since both domestic and foreign economic agents could use rupee transactions as per the Circular. For instance, the Central Bank might face the classic Mundell-Fleming issue of “impossible trinity” that highlighted the impossibility of maintaining three things, namely an open capital account, fixed exchange rate and monetary policy autonomy at the same time.

The Government of India (GoI) has to withdraw restraints on both domestic and foreign players (who would be engaged according to the Circular in settlements of their trade transactions in rupee) both in the spot or forward market. In the absence of any special arrangements/restrictions by the RBI to tackle any unintended consequences of this, monetary autonomy could be eroded. India is not a country like China who can manage their currency with capital controls due to their trade surplus as well as huge buffering of forex reserves to withstand any external shocks.

The Government of India (GoI) has to withdraw restraints on both domestic and foreign players (who would be engaged according to the Circular in settlements of their trade transactions in rupee) both in the spot or forward market. In the absence of any special arrangements/restrictions by the RBI to tackle any unintended consequences of this, monetary autonomy could be eroded. India is not a country like China who can manage their currency with capital controls due to their trade surplus as well as huge buffering of forex reserves to withstand any external shocks.

An Asian Development Bank Institute (ADBI) working paper titled as “The Benefits and Costs of Renminbi Internationalization” (ADBI Working Paper 481; Zhang, L., and K. Tao. 2014) found that in terms of the Chinese currency renminbi, one-unit rise in currency internationalisation is likely to increase the development of the financial market by 0.2 percentage points in terms of private credit and 0.7 percentage points in terms of stock market total value. This reduction in transaction costs diminishes the exchange risks of global trade and investment.

However, given the differences between the economy of China and India, and the potential risk factors, it will be better for India to adopt a gradualist approach. A RBI Staff Paper in April, 2010, titled as “Internationalisation of currency: The Case of the Indian Rupee and Chinese Renminbi” highlighted that unlike China, that normally runs a current account surplus, India generally runs trade and current account deficits.

In recent times, India has faced a downside in its external balances, especially in merchandise trade. It causes concern that fewer countries like Netherlands, Brazil, and Singapore have shown export growth for the Indian market among the top ten destination during this month. While electronic goods export has shown positive trend thanks to the thrust in domestic manufacturing, certain major exportable like gems and jewellery, engineering goods, chemicals, pharmaceuticals, and readymade garments have experienced a dip. On the import side, barring machinery and non-ferrous metals, petroleum and fertilizers have seen major growth with Russia emerging as a major source whereas the share of US, China and Australia have shown decline among the top ten major import sources for India.

Russia has acquired huge balances of Indian rupee, but Russia has not been able to use it. According to news report (Economic Times, 7 May 2023), Russian Foreign Minister Sergei Lavrov stated that Russia has huge rupee balances, but to use this amount, these rupees must be transferred in another currency, which is under discussion.

On the issue of whether India would be able to exploit benefits of rupee internationalisation, further measures would be required and the answer is uneasy since such benefits would depend on country-specific characteristics. India also needs to deepen its corporate bond market, and regulatory architecture needs to be strengthened to tackle ever-increasing financial sector sophistication. Until then, at the current level of India’s financial sophistication, there is a need for a strategic, flexible policy-oriented strategy for the rupee internationalisation in a calibrated manner.

ABOUT THE AUTHORS

Vipin Malik, Chairman, Infomerics Ratings, served on Boards of Reserve Bank of India and Bharatiya Reserve Bank Note Mudran Private Limited, Canara Bank, J&K Bank, etc. Author of several well-received books and several articles. He appears often on television debates on economy issues.

Vipin Malik, Chairman, Infomerics Ratings, served on Boards of Reserve Bank of India and Bharatiya Reserve Bank Note Mudran Private Limited, Canara Bank, J&K Bank, etc. Author of several well-received books and several articles. He appears often on television debates on economy issues.

Sankhanath Bandyopadhyay, Economist, Infomerics Ratings, has worked earlier at institutions like IIFT, CBGA, JBIC, RGCIS etc. He writes regular columns in leading media newspapers among others.

Sankhanath Bandyopadhyay, Economist, Infomerics Ratings, has worked earlier at institutions like IIFT, CBGA, JBIC, RGCIS etc. He writes regular columns in leading media newspapers among others.