Highlights

- Indian airlines currently have an order book for close to 1620 aircraft (after yesterday’s Akasa Air order, but excluding Go First and SpiceJet). This is expected to rise to closer to 2000 aircraft by Mar-2025.

- This increase will be achieved as a result of Air India converting some of its 370 options to firm orders every few months, supplemented by possible further orders by other Indian carriers.

- In 2023, Indian airlines ordered more aircraft than those from any other country. And the total order book for Western aircraft is second only to the United States.

- Developments over the last year have tracked closely in line with our expectations, with 1124 aircraft ordered in FY2024 to date, including Akasa Air’s order for 150 x 737 MAX aircraft announced yesterday.

- India is set to be the most exciting aviation market of the 21st century, with long-term rapid growth for both domestic and international traffic. However, in order to support this once-in-a-generation growth, and the eventual induction of this expanding order book, Indian aviation will need further structural and institutional reforms.

A CAPA Advisory Executive Briefing

The current Indian order book is more than 2.5x the size of the number of aircraft in service. This is by far the highest ratio in the world, reflecting the optimism about future growth.

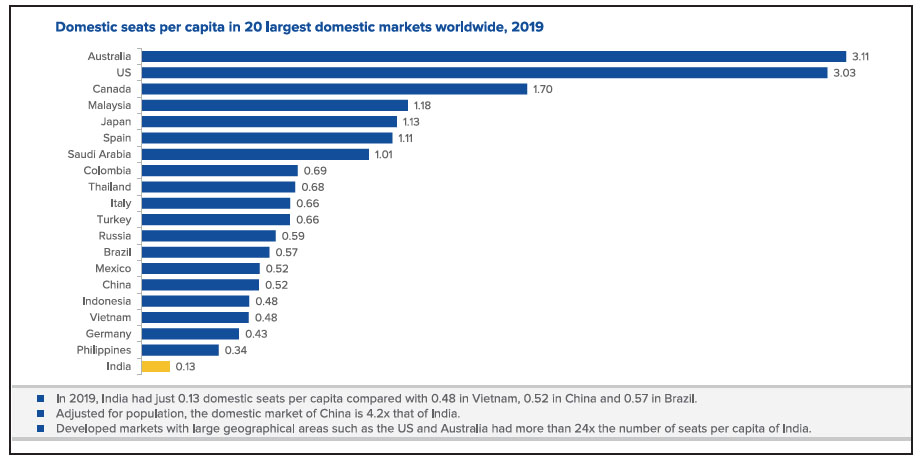

Airlines have the confidence to place larger orders because the penetration of air travel in India is by far the lowest among the world’s 20 largest domestic markets, reflecting massive upside potential.

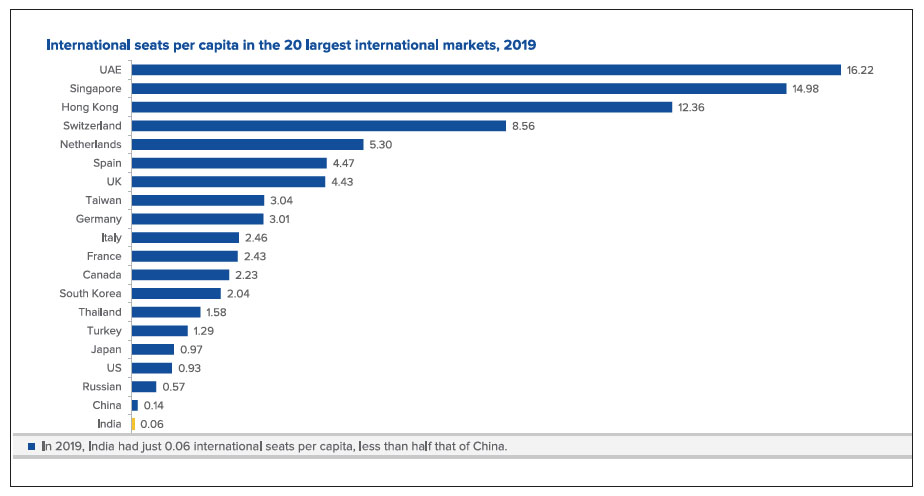

Similarly, in terms of international seats per capita, India is well below other large aviation markets. The long-term fundamentals for continued growth remain very strong. We have only just scratched the surface.

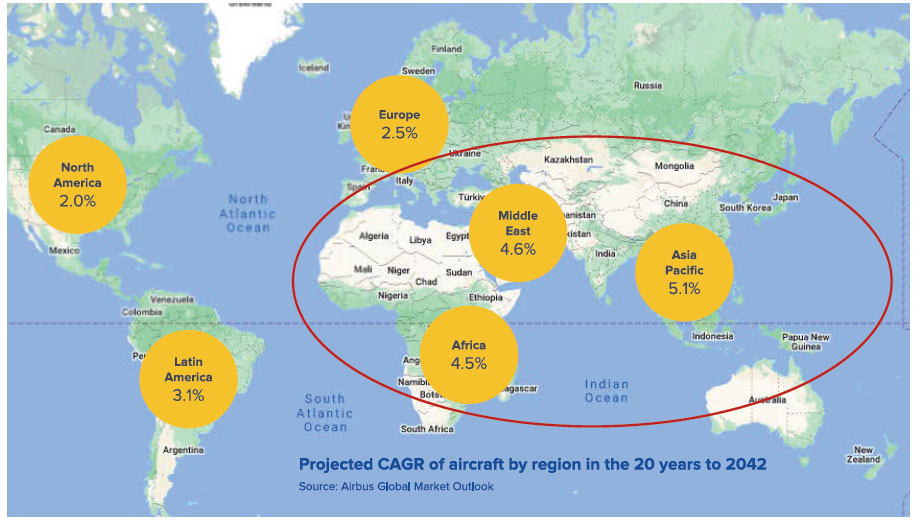

The centre of gravity of global aviation is moving eastwards. Asia, the Middle East and Africa are expected to drive 67% of worldwide fleet expansion over the next 20 years.

India has a unique opportunity, positioned at the epicentre of this global aviation growth. In addition to its massive home market, among the five leading aviation markets in the world India has arguably the most favourable location to act as a hub on the fastest growing intercontinental corridors.

India is in a unique position, in terms of scale, growth and geography. It will need to decide what kind of aviation market it seeks to be and chart a path towards achieving that. Other major markets may not have a similar combination of positive attributes to be comparable benchmarks to follow.

- India has a unique opportunity, being the world’s fastest growing market, and positioned as it is at the epicentre of global aviation growth. [see next two slides]

- In addition to its massive home market, India has arguably the most favourable location among the five largest aviation markets in the world (the others being the US, China, UK and Japan), to act as a hub on the fastest growing intercontinental corridors:

- The geographic location of the US as an end-of-the-line market means that it has limited opportunities to serve as an international hub.

- India may reach the size of China within 12-15 years. But China has an aviation industry that has a high degree of central government control and planning, which is not the case in India.

- Both China and Japan have location that limits their hub potential to trans-Pacific routes.

- The UK has the ability to handle traffic to/from North America and Europe, which is certainly large in volume. But these will also be the slowest growing markets going forward.

- Australia, as has been shown, is the most similar to India in terms of market concentration. But by the end of this decade, India’s market will be almost 5x the size of Australia, making parallels between them less relevant. And Australia too is an end-of-the-line market.

- India is therefore uniquely positioned, being the third largest, fastest growing and one of the most favourably located markets to be able to handle a massive home market and hub traffic. India will need to decide what kind of market it needs to be, and a robust institutional framework then needs to be developed with this in mind.

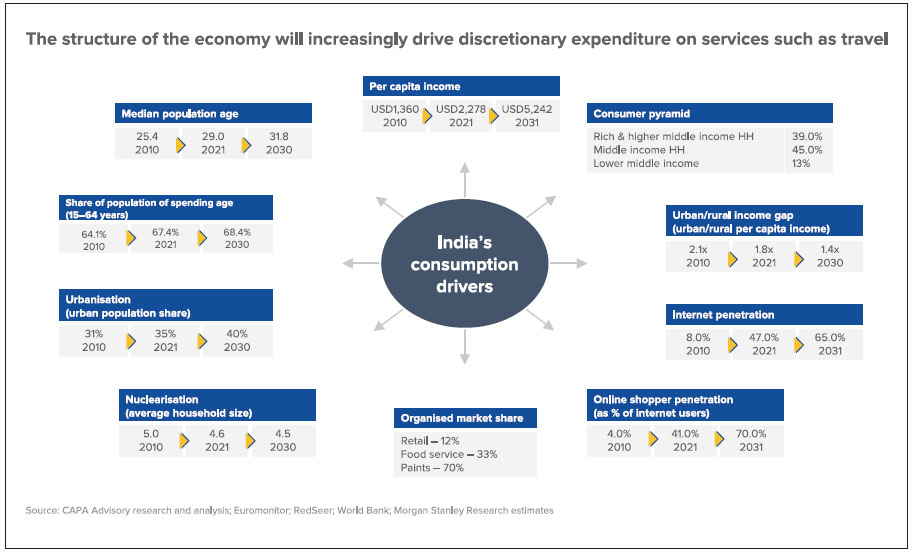

India’s economy and demographics are experiencing underlying structural changes that will have a positive and material impact on economic growth, and by consequence on air travel.

Home to top 10 fastest growing cities

- The World Economic Forum projects that all of the top 10 fastest-growing cities in the world during 2019–2035 will be in India.

- India’s dominance indicates the broader theme of the tipping of global economic activity from the West to the East.

Uptrend in share of global trade & merchandise exports

- India’s of merchandise exports increased from 0.6% in the early 1990s to 2.4% in 2022.

Urbanisation trends

- The UN projects 68.0% of the world’s population would live in urban areas by 2050, up from the current 55.0%. This implies an addition of 2.5 billion people to the urban count.

- In 35 years (1980–2015), the urban population in India increased by 268.0 million. The urban population is projected to increase by 448.0 million during 2015–2050.

The Fourth Industrial Revolution

- The Fourth Industrial Revolution (4IR) has the potential to transform economies such as India by tackling some large-scale systemic challenges.

- The 4IR provides an opportunity to transition from a low value-added services economy to a strong, R&D-driven products and innovation ecosystem.

- India is well-poised to lead the 4IR, given the presence of a young population that is technologically sound, a large educated labour market and a better IT ecosystem. Also, it is well poised to leverage opportunities created by the growth of 4IR technologies.

The structure of the economy will increasingly drive discretionary expenditure on services such as travel

India’s middle- and upper-income categories are growing the fastest. The number of households earning more than USD35,000 per annum is projected to grow at a 10-year CAGR of 16.2% through to 2031.

Managing the massive, once-in-a-generation growth that is expected, will not be possible without a complete re-think of India’s physical, institutional & skills infrastructure. We have a window of around 5 years to address these issues, and need to start immediately, failing which risks will otherwise increase.

Key areas that will require reform and attention

Aviation regulation

- The DGCA should be recast along the lines of the CAA UK. An independent and professionally-managed safety regulator is essential.

Security regulation

- The Bureau of Civil Aviation Security needs to be re-cast as an independent, technology-driven security regulator, modelled on the Transportation Security Administration.

Airport regulation

- Given the changing aviation landscape, including for example, the emergence of dual airport systems and their implication for competition, a new AERA Act is required.

Air navigation services

- Air navigation services should be corporatised to be able to invest in sufficient capacity, efficiency and safety to meet long-term requirements. This has been pending for many years.

Skills & training

- Our aviation skills and training infrastructure needs to be overhauled across the board, including flight training organisations, simulator centres, maintenance training academies, air traffic controller training, cabin crew academies and the delivery if regulatory and security training.

Consumer and competition issues

- Competition and consumer issues need to be given appropriate consideration and protection, irrespective of whether or not there is market concentration.

Airport infrastructure

- A long-term plan needs to be developed for airport capacity, with a planning horizon that extends beyond the next 5-7 years for a generation or more.

Fiscal regime

- And arguably most importantly, the negative fiscal regime must be addressed. Indirect taxation currently accounts for close to 20% of airline revenue and must be fundamentally re-aligned to support viable operations.

Bilaterla policy

- India will require a clearly-defined international air services strategy and bilateral policy that balances the interests of Indian carriers with India’s overall connectivity requirements.

India is forecast to see domestic traffic rise to 300-350 million passengers, and international traffic to 140-160 million passengers by FY2030, and may further almost triple by FY2043, by which time it will be larger than the US market today.

Indian scheduled airlines are likely to operate a fleet of 1,400 aircraft by FY2030. By FY2043 the fleet size is expected to approach 4,000 aircraft, comparable to China today. (Indicative only for strategic reasons)

But in the short-term, the industry will need to handle a couple of critical challenges for the next 1-2 years. In addition to serious ongoing supply chain issues, airlines now have to deal with the impact of the revised Flight Duty Time Limitations.

- Supply chain issues are serious and will remain a concern for the foreseeable future. There are currently 160 aircraft on the ground, which could increase to around 200 by the end of Mar-2024, representing almost 25% of the aircraft on the register. There is continuing uncertainty since nobody can determine the timeframe by which these issues will be resolved, nor rule out the possibility of further issues emerging.

- The recent revisions to the Flight Duty Time Limitations may result in airlines having to increase their pilot numbers by closer to 20% in order to be able to remain compliant with operating the current schedule, let alone future growth. And this is happening at a time when there is a structural global shortage of pilots. Indian carriers will be competing with expanding airlines in the Gulf and Asia in particular, for a constrained pool of pilots.

- Compliance with the new regulations within the timeframe provided will be a challenge. This could result in increased flight cancellations and a further deterioration in on-time performance, and may have an impact on network planning.

- FDTL issues will have critical operational and financial implications from Summer 2024, especially given the growth that is expected.

Indian aviation is experiencing structural tailwinds – for the first time since the industry was deregulated in the 1990s – which the industry must take advantage of.

- Almost 30 years after deregulation, and 20 years since the second phase of liberalisation, for the very first time we have a strong and well-capitalised airline system, with the balance sheets required to support the growth potential of the market, and the determination to be world class operators.

- Indian aviation has, possibly for the first time, airport capacity either in place or under development that exceeds projected demand for the next 5-7 years. Metro airports are expected to have a structural capacity of around 500-550 million passengers. And even Adani Airports’ six non-metro airports will also see significant expansion of capacity ahead of demand, with eventual masterplan capacity of close to 200 million passengers.

- Dual airport systems in Delhi and Mumbai will be game-changing for the industry and the economy.

- Recent air navigation initiatives such as the expansion of airspace available for flexible use, and the halving of lateral separation for aircraft are positive developments

- However, the pace of growth will be at a once-in-a-generation level. This will require radical changes not seen before in India, to arrive at a new order in terms of physical, institutional and skills infrastructure.

- The Ministry of Civil Aviation clearly recognises this. It has been proactive in delivering many positive initiatives already and is aware that deeper institutional changes are required.

ABOUT CAPA INDIA

![]() CAPA India was established more than 19 years ago with a mission to become a leader in global aviation knowledge. We have since built a worldwide portfolio of clients and experience, and an enviable reputation for independence, insight and integrity. Today aviation businesses around the world turn to us for sound advice and research.

CAPA India was established more than 19 years ago with a mission to become a leader in global aviation knowledge. We have since built a worldwide portfolio of clients and experience, and an enviable reputation for independence, insight and integrity. Today aviation businesses around the world turn to us for sound advice and research.