Structural challenges that historically constrained India’s international market are gradually being dismantled, allowing a transformative landscape to emerge.

FY2000 to FY2010

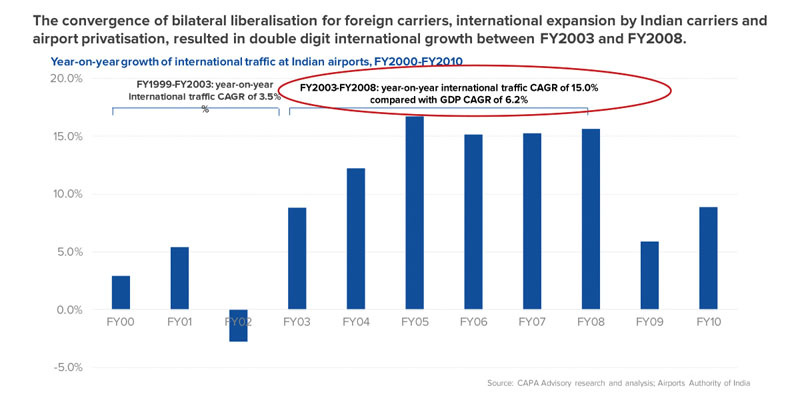

- A period marked by a dramatic shift from a virtually closed market to a very liberal regime, complemented by increasing international activity by Indian carriers.

FY2000-FY2004

- Until FY2004, Air India/Indian Airlines were the only home carriers permitted to operate international services. But they did not have the fleet nor commercial inclination to pursue active international expansion.

- Meanwhile, for foreign carriers, India had arguably one of the most restrictive market access regimes in the world. Carriers such as Virgin Atlantic ended up having to pay royalties to ‘sub lease’ Air India’s entitlements because of BASA limitations.

FY2004-FY2010

- From FY2004 onwards, a very liberal market correction took place due to a strategic convergence of key elements for change.

- Air India placed an order for 111 aircraft, including 50 widebodies.

- Kingfisher placed orders for around 25 widebodies, including 10 A380s.

- Jet Airways inducted 20 widebodies (plus options for 10 x 787s) and tens of narrowbodies in a very short period of time after being granted permission to operate international services, 10 years after it launched. Jet had a world class product, a strong brand and a loyal customer base.

- Bilaterals were liberalised, with a close to 300% increase in seat entitlements with key markets, along with an Open Skies agreement with the US, and a near Open Skies agreement with the UK.

- Simultaneously, airport privatisation and modernisation changed the face of Indian aviation, with the development of international standard infrastructure at Delhi, Mumbai, Bangalore, Hyderabad and 35 AAI airports.

- Growth was achieved despite the 5/20 rule which was the most negative regulation ever introduced in India.

- This positively changed the proposition for customers, providing more choice and more attractive fares, stimulating both inbound and outbound traffic.

The convergence of bilateral liberalisation for foreign carriers, international expansion by Indian carriers and airport privatisation, resulted in double digit international growth between FY2003 and FY2008.

FY2010-FY2020

This decade saw a convergence of events that resulted in a reversal of conditions with a virtual freeze on bilateral liberalisation for foreign carriers, while financial losses in the domestic market impacted the ability of Indian carriers to expand overseas.

- Could not capitalise on its modern fleet as the inflight product remained sub-standard, maintenance of cabins was poor, aircraft were on the ground, it was losing relevance in the market, and incurring serious red ink. Air India’s membership of Star Alliance was deferred and was not fully leveraged.

- After aggressive international push to JFK, Newark, Toronto, San Francisco and Shanghai, realised that its balance sheet could not support this. This was driven by the costly acquisition of another airline which starved them of funds at a critical time.

- Growth slowed, very high product quality standards were compromised, options for 787-9s were not converted, and the carrier became more of a regional arm of Etihad.

- After a promising start with a world class service to London, the airline closed in 2012.

- Bilaterals were largely frozen with a couple of exceptions:

- Abu Dhabi in 2013, in relation to Jet Airways deal

- Dubai in 2014, which provided for a 20% increase

- Oman and Saudi Arabia, but their carriers were not really carrying much traffic to Europe and North America

A missed opportunity

- During this decade, GDP almost doubled, and the absolute increase in per capita GDP was 3x that in the previous years. Meanwhile the diaspora market continued to expand with increasing migration. But the potential of the market was not realised.

- In FY2000, India’s international traffic was actually slightly higher than domestic. By FY2020 it had become less than half.

During the period FY2010 to FY2020, international traffic grew at a CAGR of just 6.8%, far more moderate than earlier due to a freeze on bilaterals and the inability of Indian carriers to provide capacity.

FY2024-FY2030

Back to the future. Favourable conditions are once again aligning, as they did during FY2003 to FY2008. But this time, the airline industry is much stronger and the economy is much larger.

Indian carriers have strong balance sheets, patient capital and a strategic determination to build world class airlines

- Privatisation will result in India having a capable and well-capitalised network carrier, supported by a large fleet order for 470 aircraft, including 70 widebodies. India will finally have a full service airline with a state-of the-art fleet suitable for all missions, world class product and service, and an expansive network. First time since deregulation in the 90s that an Indian airline has formidable ability to fund a very aggressive business case.

- With its order of close to 1000 aircraft (which includes A321XLRs, possibly to be joined by widebodies in future), combined with an existing fleet of 339 aircraft, IndiGo will be very strong on short and medium haul routes.

- The carrier has a very strong balance sheet and has the ability to further infuse long-term capital if required, and a brand and network that will make it a formidable competitor.

- International services will debut in 2024 and will help to de-risk its domestic operations.

Indian carriers are expected to deploy an additional 325-350 aircraft on international routes over the next 5-7 years

Other factors contributing to a positive outlook for international growth

- Economic Growth: Strong economic growth and rising prosperity, especially among the addressable market will drive increased demand for travel.

- Airport Capacity: For the first time airport capacity is being developed ahead of demand, with 500 million passengers of capacity in the pipeline. Three cities will have dual airports.

- Hub Development: Airlines and airports are both focusing on the development of hubs, to leverage domestic connections, but also to take advantage of India’s geographical location to capture South Asia traffic, and in due course intercontinental transfers – if required.

- Bilateral Policy: CAPA Advisory expects that the bilateral regime will start to open up from FY2025, perhaps modestly and gradually to begin with.

Double-digit growth cannot be taken for granted, but the conditions are as favourable as they have ever been in the Indian aviation sector.

Growth will inevitably face challenges…

- Supply chain issues impact aircraft and engine deliveries – could turn serious and may constrain growth.

- Availability of pilots and skilled workforce. There is likely to be a serious fight for commanders from this fiscal.

- Institutional capacity building at the DGCA and BCAS.

- Management capital to handle the complexity of rapid growth.

Continuation of the negative fiscal regime.

- Ability of airspace capacity to keep pace with growth.

- Geo-political tensions and possible continuing uncertainty.

We believe that the positive macro environment will outweigh these issues in the long-term, although this remains to be seen

- Consumers will for the first time have a choice between world class Indian FSCs and LCCs and leading global carriers.

- Which is why CAPA Advisory believes that international is suddenly the new domestic.

Based on CAPA India’s periodic coverage and research since 2011, we believe there is a need for setting up the right foundation for sustained profitable growth.

Challenges for travel businesses

- There are many India’s in one India

- India is an extremely heterogenous geography with diverse cultures, ethnicities, languages (121 languages spoken by 10,000 or more people), beliefs.

- One “fit for all” approach will not generate business results to the extent required

- Do not presume the approach that has worked for the business elsewhere will be successful in India

- Generic campaigns, even with powerful testimonials or star power, will not appeal to the “many India’s”

- Shah Rukh Khan (Hindi) vs. Rajnikant (Tamil) vs. Diljit Dosanjh (Punjabi) vs. Mitra Gadhvi (Gujarati) vs. Manoj Tiwari (Bhojpuri)

- Generalizations result in less effective campaigns

Solutions

Requires a much deeper and qualified understanding of:

- The Market: which is very dynamic and rapidly evolving

- The Consumer: Demographics (income is reconfiguring from the shape of a pyramid to a diamond), and psychographics

- Competition: Competitive intensity, options

- Distribution: Quality, reach, incentives

- Point of sale: Opportunity, profitability, potential.

- Pricing: What is the consumers real ability to pay? Strategy (value vs. experiential vs. commoditised offerings)? Could leisure generate higher yields in future?

Enabled by

- On-ground, real-time research across the travel ecosystem – consumers, markets, airlines (incl. networks), travel agents, tour operators, regulators, airports (incl. networks)

- Digital and data tools/capabilities

- Proprietary models

India is set for game-changing international air connectivity. Indian carriers are likely to launch new routes to destinations across the world…in Australia

New route opportunities for Indian carriers exist across the globe – including for example (and these are indicative only), destination such as Boston, Dallas, Houston, Los Angeles, Athens, Barcelona, Budapest, Geneva, Manchester, Prague, Warsaw, Zurich, Cairo, Johannesburg, Lagos, Marrakech, Seychelles, Amman, Beirut, Medinah, Neom Bay, Red Sea, Tehran, Beijing, Guangzhou, Hanoi, Ho Chi Minh City, Langkawi, Manila, Phnom Penh, Siem Reap, Brisbane and Perth.

Global regions such as South America, the Caribbean, Africa and the Pacific, that are less likely to see direct connectivity will be served by alliance partners and extensive codeshare arrangements.

Connectivity is likely to flow as follows:

- South America via European hubs such as London, Paris, Frankfurt and Madrid

- Caribbean via US hubs such as New York JFK, Newark, Dallas and Houston

- Pacific via Australian hubs such as Sydney, Melbourne and Brisbane

- Africa via African hubs such as Cairo, Lagos, Nairobi and Johannesburg

High-volume routes that are currently served will see significant growth in frequencies, as well as connectivity from more Indian cities.

- US, UK and high-volume short haul markets will be served from multiple metros

- Australia, Canada and Continental Europe will primarily be served from Delhi, Mumbai and possibly Bangalore.

India’s Tryst with Foreign Travel

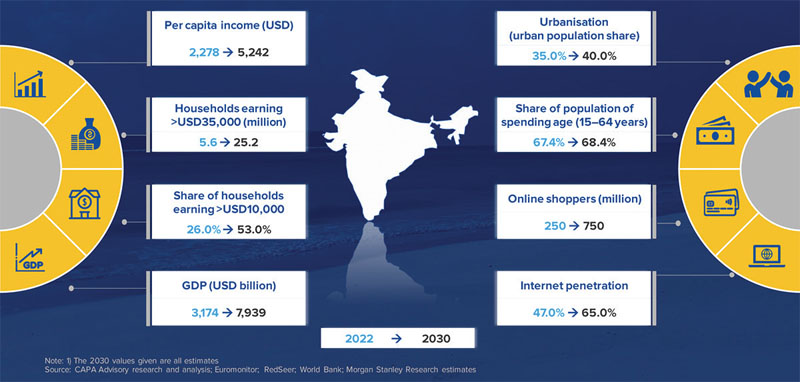

India is going through a structural transformation of its key economic and consumption drivers. The addressable market for travel will grow much faster than the national average providing impetus for higher-end travel.

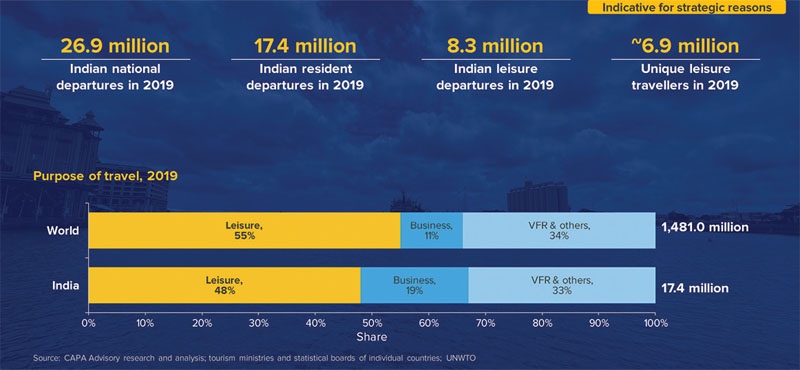

Departures by Indian nationals were reported to be 26.9 million in 2019. However, the number of Indian resident departures was almost 35.0% lower at around 17.4 million.

Leisure accounts for a lower percentage of India’s outbound travel relative to the global average, and even this figure is believed to be over-stated as it includes an element of VFR travel, which is likely higher than what the current data indicates.

The Indian leisure outbound traffic could potentially grow to 28.1 million by 2030. International leisure expenditure would increase to USD 65-75 billion from the current 16-18 billion, of which 20% will be the expense on airfares.

Indian carriers will have greater flexibility when assessing the commercial potential of new routes, because of the ability to tap into connecting traffic on intercontinental corridors. By FY2030, this is expected to be an addressable market of up 100.0 million passengers.

- As of 2019, the potential I-I market for Indian carriers on intercontinental corridors that can be reasonably connected via India was around 80.0 million annual passengers. This is expected to reach 100.0 million by FY2030.

- This may not be a primary focus for Indian carriers, given the strong home demand. But it does provide the ability to open up supplementary traffic flows during seasonal dips on the core route.

- This can significantly enhance the viability of leisure routes, which may see more season fluctuation in demand.

In Conclusion

- India is witnessing a unique convergence of strong macro factors which can create long term structural shifts.

- Serious investment will occur in international connectivity across segments – short- medium- long- and ultra-long-haul.

- India will for the first time have a world class long-haul airline, in Air India, with the right network, fleet, product, and service.

- India will also have a world class short- and medium-haul airline, and potentially long-haul, in IndiGo, with the right network, fleet, product, and service.

- Bilaterals cannot be, and should not be, held up for long, CAPA Advisory expects gradual opening up from FY2025, allowing market forces to play a decisive role.

- The Indian economy will see a transformation – GDP likely to grow from USD3.5 trillion to USD7-7.5 trillion, GDP per capita expected to grow from USD2,200 to USD5,500 by 2031. As such the overall addressable market is expected to expand and become much larger.

- Airport infrastructure is, for the first time, being developed ahead of demand – additional annual capacity of 500 million passengers is planned. Furthermore, there is a focus on developing strong gateways/hubs.

- The tremendous potential that exists still needs to be converted and will require a strong understanding of the consumer, including demographics and psychographics, supported by continuous investment in researching traveller behaviour and preferences, distribution, point of sale, pricing, marketing effectiveness etc. to enable data-driven decision making.

- Airports will similarly have to adapt their retail, duty-free, and F&B formats to align with the rapid evolution of the customer. By FY2030 India’s international bidirectional traffic will reach 140-160 million passengers (70-80 million departing).

Outbound resident departures are expected to account for over 50 million, of which more than 28 million will be for leisure. That represents a more than 3x increase in outbound leisure travellers. But this needs to be realised, and be realised at sustainable yields.

ABOUT CAPA INDIA

CAPA India was established more than 19 years ago with a mission to become a leader in global aviation knowledge. We have since built a worldwide portfolio of clients and experience, and an enviable reputation for independence, insight and integrity. Today aviation businesses around the world turn to us for sound advice and research.

CAPA India was established more than 19 years ago with a mission to become a leader in global aviation knowledge. We have since built a worldwide portfolio of clients and experience, and an enviable reputation for independence, insight and integrity. Today aviation businesses around the world turn to us for sound advice and research.